Mapping Aerospace M&A

In mature industries like aerospace and defense, mergers and acquisitions are primary tools of corporate strategy. As the bases of competition for product and service offerings become ever more firmly established, the race for competitive advantage increasingly relies on initiatives to reshape the scale, scope, and vertical depth of a company’s structure. More specifically, corporate development initiatives are how mature-industry firms adapt to change—inflections in demand, perturbations on the landscape of technology, capital markets, politics, etc.

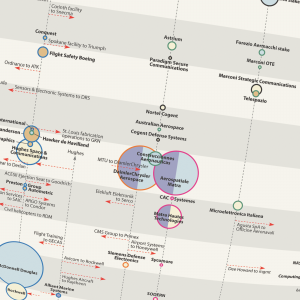

These principles come vividly to my mind as I consider the a new map of Aerospace, Defense, & Government Services–Mergers & Acquisitions (January 1993 – December 2016), which we have published today.

The document expands and updates a well-regarded infographic from the 2000s, which we have revived in a partnership with Renaissance Strategic Advisors. The Map depicts the mergers, acquisitions, divestitures, and major recapitalizations that comprise the 25-year lineage of two dozen leading companies in our industry. Each transaction’s rendering on the Map indicates its date and value as well as the sectors in which the acquired businesses participate and the nationality of their home markets. The resulting array of images puts a distinctive face on the deal making that has remade aerospace companies and restructured the industry.

Six years past the 2010 inflections marked by the Great Recession’s bottom and Iraq War’s end, what are the story lines of corporate development that stand out on this Map?

- It is easy to see how the historic growth in orders and deliveries of large commercial airliners that accompanied recovery from the financial crisis has been reflected in M&A. The two largest transactions of the past six years—United Technologies’ 2012 acquisition of Goodrich for $18 billion and Berkshire Hathaway’s buyout last year of Precision Castparts at a valuation of $37 billion—both share an impetus in these commercial-aero boom years. That same impetus also underlies the appearance on the Map of several comparatively smaller transactions—GE acquisition of Avio Aero in 2013, Safran’s acquisition of the RTM322 engine business that same year, and Rockwell Collins’s pending acquisition of B/E Aerospace.

- The downdraft in Pentagon investments that began in 2010 has had an equally profound effect on companies occupying that sector of the market, whose responses show up on the map as a flurry of dotted red lines signifying spin-outs and divestitures. Three distinct themes animate these “portfolio-shaping” initiatives. First, there have been multi-billion dollar divestitures by diversified companies curtailing exposure to declining and volatile defense markets, a theme punctuated by United Technologies’ sale of Sikorsky to Lockheed Martin in 2015, the separation of ATK in 2015 between its defense/aerospace businesses and Vista Outdoors, a commercial sporting goods company, and Airbus’s sale of its defense electronics business to the private equity firm KKR earlier this year. Second, some of the defense companies themselves—Lockheed Martin and L-3 Technologies, most notably—have been exiting the information technology and services segments of the federal market. Finally, the decline in defense spending gave impetus to a slew of divestitures tightening the focus of a company’s business and financial model (e.g., Northrop Grumman’s 2011 spin-out of its shipbuilding sector as Huntington Ingalls)

- Viewed in the context of a full quarter-century of M&A activity by aerospace and defense companies, the comparative paucity of deal making since 2010 also stands out, particularly among the largest companies. With the exception of Lockheed Martin, which has cultivated a steady agenda of strategic transactions over the past six years, none of the other “big-six” US defense contractors has made an acquisition larger than Raytheon’s $1.6 billion acquisition of Websense in 2015. Honeywell, the third highest-valued company on the Map, has made only four small aerospace transactions in six years, and went fully three years, from 2012 to 2014, without making a single acquisition in its aerospace businesses. Boeing has made 10 acquisitions in six years, but no one of which exceeds the $106 million it paid for Miro Technologies in 2012.

That last observation may bear an ironic tone, but it’s not a criticism. After all, the robust valuations which nearly the entire industry enjoys today are some kind of testament to the merit in the general corporate development initiatives that have prevailed since 2010. At the same time, for all that it may illuminate about how our industry has employed M&A to adapt to change, the Map reveals little about where these story lines may lead beyond the next inflection.

Leave a Reply